Backtesting research

Why Market-Level Backtesting Matters More Than One Great Chart

Learn why a strong backtest on one stock is only a starting point, and how broader forward-style testing can reduce overconfidence.

One stock can make an idea look far more reliable than it is.

The chart is clean. A seasonal window has worked repeatedly. The annual returns look attractive. That is enough to make an idea worth researching, but it is not enough to conclude that the underlying rule is robust.

The next question is broader: does the logic still make sense when it is applied consistently across a wider market and tested without using information from the future?

This is where market-level backtesting matters.

A strong ticker is a starting point

Single-stock research is useful. It is how most ideas begin. You find a company, define a historical window, review the annual outcomes, and decide whether the pattern is interesting.

But a single example has limitations. The result may be shaped by one company’s unusual growth cycle, an acquisition, a sector boom, or a small number of unusually strong years. The pattern can be real and still be too narrow to support a broad conclusion.

When the same selection rules are applied across a defined universe, what held up over time?

That changes the object of study. Instead of searching for the most persuasive chart, you are examining a process.

Every backtest result is one defined question

A result is never “the answer.” It is the answer to one specific configuration.

The market universe, lookback history, test year, long or short direction, probability threshold, holding period, and number of positions all matter. Change any of these inputs and you are testing a different rule.

That is why a backtest grid should be read as a map of research choices, not as a scoreboard. A strong cell can be useful, but it needs to be examined: how many signals were included, how large was the drawdown, how concentrated were the returns, and did the result remain credible outside the period that selected it?

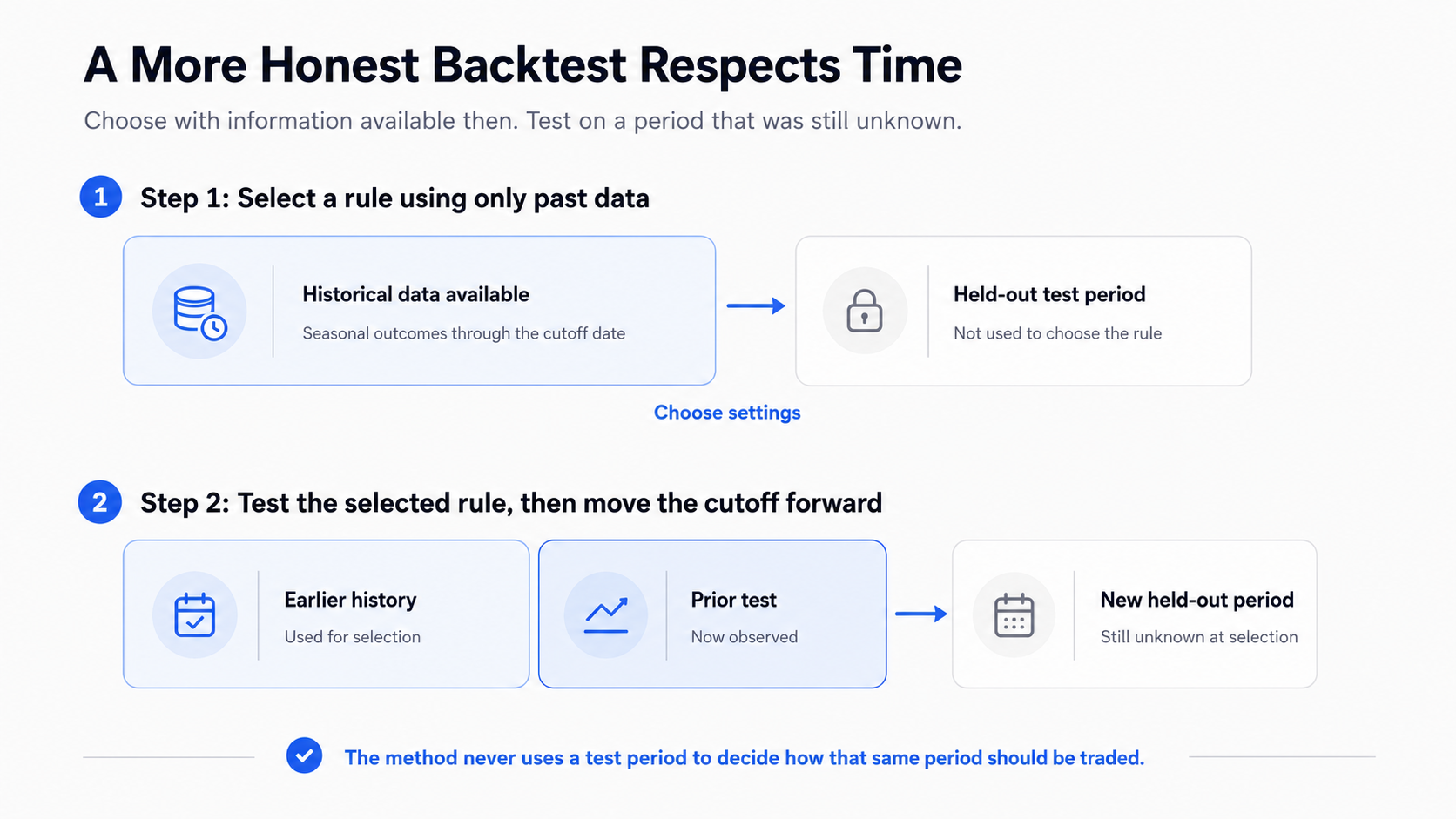

Respect time: test tomorrow with yesterday’s information

The most important safeguard in historical research is simple: do not let the method learn from the period it is later judged on.

In a forward-style or walk-forward test, the statistics used to select a configuration are calculated only from data available before the test year. The selected rule is then evaluated on the following period, which was not part of the earlier calculation.

This does not guarantee a future result. It does make the historical exercise more honest.

If a model can see future outcomes, even indirectly, the result can become a reconstruction of what would have worked with hindsight. The numbers may look precise, but the test is flattering the method rather than challenging it.

Look past total return

Total return is easy to quote and easy to overvalue. A better evaluation also includes:

- Number of trades or signals.

- Win rate and average outcome.

- Largest gain and largest loss.

- Maximum drawdown.

- Average holding period.

- The shape and stability of the equity curve.

- Whether results are concentrated in a few periods.

A result can look excellent in one summary metric and still have a drawdown or concentration profile that makes it difficult to use in practice.

Broad testing does not create a magic setting

A market-level test can reduce the chance that you are attached to a single appealing anecdote. It cannot discover a permanent setting that will work in every regime.

The best use of broad testing is to identify configurations that deserve closer inspection, then ask why they worked and where they failed. A rule that is only attractive in the summary but breaks down under small changes is less convincing than a modest rule that remains understandable across different samples.

A practical research sequence

- Start with a ticker or market idea.

- Make the dates, universe, and rules explicit.

- Inspect the individual historical result.

- Test the same logic across a broader defined universe.

- Keep the evaluation period separate from the data used for selection.

- Review drawdowns, trade count, and weak periods before trusting a headline return.

MarketOdds is intended to support this kind of research: historical context first, conclusions second. Explore an individual ticker in Ticker Analysis, then review broader setups in Opportunities.

Look at the window, not just the headline.

Compare seasonal history for a stock you already follow, then decide whether the context is worth further research.

Historical patterns describe past market behaviour. They do not predict future returns and are not investment advice.